From Ticket Reservations to Phones as Tickets and Money -- Part 2

Back to Contents of Issue: August 2002

|

|

|

|

by Jeffrey L. Funk |

|

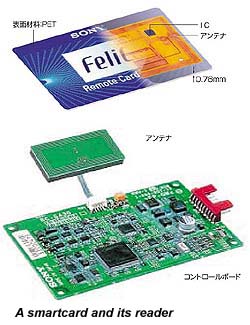

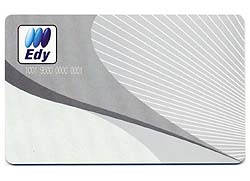

LAST MONTH WE LOOKED at the impact JR East's Suica smartcard is having in the Tokyo area. The next step in the evolution of tickets is to put the appropriate train ticket smartcard functions in the mobile phone. Does NTT DoCoMo's announcement that it will put Bit Wallet's electronic money, called Edy, in its phones include plans to incorporate JR East's smartcard ticket capability? The answer is currently unclear, but the compatibility between Suica and Felica, the smartcard version of Edy, suggests it would not be very difficult to do so. LAST MONTH WE LOOKED at the impact JR East's Suica smartcard is having in the Tokyo area. The next step in the evolution of tickets is to put the appropriate train ticket smartcard functions in the mobile phone. Does NTT DoCoMo's announcement that it will put Bit Wallet's electronic money, called Edy, in its phones include plans to incorporate JR East's smartcard ticket capability? The answer is currently unclear, but the compatibility between Suica and Felica, the smartcard version of Edy, suggests it would not be very difficult to do so.For train lines, the benefits of combining Edy and Suica include lower card costs. For smartcard commuters, the benefits include easier recharging, better security and viewing of the current balance. As opposed to recharging their cards in the train stations with cash, users should be able to recharge the phone anywhere using a credit card or bank account number. And while the current balance is not easily read on the Suica card, this would be easy to do with the mobile phone. Putting the train ticket smartcard function in phones will also provide users with more security. Passwords and other forms of user identification could be included in the phone, thus making it more difficult for someone to use another person's ticket or electronic money. Currently, smartcards are like money and thus if they are stolen, the user cannot quickly cancel the card or be reimbursed as with a credit card. The security advantage and the convenience of having the smartcard in a phone may reduce the barriers to adoption. The initial problems of putting train ticket smartcard functions in the phone are cost and technical issues. The smartcard has very high production volumes while initially the mobile phones with smartcards will not. Technically, while the Suica card itself acts as an antenna, the mobile phone will require a special antenna for communicating with the card reader. Further, the phone will require a stronger signal (and greater battery power) due to interference between parts inside the phone and the existence of the shield; problems that don't now exist when someone places their card over a reader. Of course, NTT DoCoMo's decision to adopt Edy may mean that it is well on its way to solving these problems. The bigger challenge, however, is finding agreement between the rail lines and NTT DoCoMo. Key issues include who owns the information on the train ticket users, who manages customers and who decides on the rules for tickets. This problem is slightly complicated by the capital linkage between JR and J-Phone. Apparently NTT DoCoMo wants the train lines to match their services with its technology while the train lines are more concerned with their customer needs. In the end, customers will decide whether putting train ticket IC functions in phones and using smartcards for train tickets are good ideas. That's entertainment It has been possible to purchase and reserve event tickets such as concert tickets on the phone and online in many countries for years. In the US, Ticketmaster and Ticketron have been the leading providers of these tickets, while Pia has been the leader in Japan since it began publishing magazines that contained information on concerts and other parts of the entertainment industry in the mid-1970s. In 1980, it became the first Japanese firm to include seat information in computers, which eliminated the inventory management problem associated with physical tickets. Ticket sellers in Japan and other countries make money through commissions and other fees. In Japan, they receive commissions from event promoters that represent between 5 and 15 percent of the ticket price. Some ticket sellers also charge users a fee for each sale -- for example, E-Plus, the largest seller over the Japanese Internet, charges users JPY350 for sales over the Internet and JPY450 on the phone. Unlike Ticketmaster and Ticketron, Pia and other Japanese firms were relatively slow to begin providing Internet-based services. Pia was slow because it has been concerned about losing magazine sales, which, as of early 2001, still represented a larger percentage of its income. It started its PC Web-based services in 1997 when overcrowded phone lines raised concerns about lost sales. Lawson, a convenience store chain, began taking reservations over the telephone in 1996 in cooperation with several concert promoters that saw Lawson's convenience stores as a useful place for consumers to pick up and pay for tickets. Lawson later started PC Internet services. In February 1999, Lawson and Pia began offering i-mode concert ticket services. Although Lawson was quicker than Pia to expand the breadth of its products, Pia had done this by the end of 1999 and appears to have caught up with Lawson in terms of i-mode sales by sometime in 2001. E-Plus, a partly owned subsidiary of Sony, was the last firm to start PC and mobile services in April 2000. Although it emphasizes Internet sales more than the other firms since it does not have ticket outlets like the others, it has placed less emphasis on mobile than PC Internet services. Pia is still the leader in ticket sales but it has been slower to move to the Internet than Lawson or E-Plus. Estimates of the share of tickets sold over the Internet range from 10 to 20 percent and depend on the ticket seller and one's definition of which ticket types to include in the estimate. Concerts frequented by young people have a much higher percentage of Internet sales than do classical or jazz music, theater or sports tickets and thus represent the first potential event application for smartcards. Event tickets that are ordered by telephone or online are either delivered or the buyer picks them up at a specific location. Rock concerts particularly those in Japan have special characteristics: First, some young people do not have credit cards or bank accounts and they often do not want to ask their parents to purchase the tickets for a variety of reasons. Thus, they must pay for and pick up the tickets at a specific location. This provides firms like Pia and Lawson with a strong advantage since they have many ticket outlets.  Second, many rock concerts sell out very quickly, so ordering by telephone only helped a little as many people were forced to spend many hours waiting on the telephone. The PC and mobile Internet has partially solved this problem and created a set of new problems. Japan's Internet ticket sellers enable people to register for lotteries where winners receive the right to purchase tickets. The lottery winners then have a certain amount of time to purchase the tickets (typically one week) before their rights are cancelled.

Second, many rock concerts sell out very quickly, so ordering by telephone only helped a little as many people were forced to spend many hours waiting on the telephone. The PC and mobile Internet has partially solved this problem and created a set of new problems. Japan's Internet ticket sellers enable people to register for lotteries where winners receive the right to purchase tickets. The lottery winners then have a certain amount of time to purchase the tickets (typically one week) before their rights are cancelled.Although all three ticket sellers provide this lottery service to users, Pia and Lawson have created Internet and telephone purchasing processes that make the best of their ticket outlets. Users can receive a code number when they reserve a ticket on the Internet or on the phone. In the case of Lawson, users input this code number into a kiosk in a Lawson convenience store to receive a ticket, which they pay for at the register. Pia uses a similar system in its ticket outlets and in conjunction with convenience stores. The use of these code numbers and the delay between reserving and paying for tickets can cause problems for ticket sellers and promoters since some people, particularly scalpers, will register for many lotteries under various names and thus win the rights to purchase many tickets. If the concert is popular, they sell the tickets for very high prices, which can annoy the real customers who merely want to see the concert. The bigger problem occurs when the concert turns out not to be popular and the scalpers do not exercise the right to buy tickets thus leaving many tickets unsold at the last minute. Introducing smartcards It is expected that smartcards will solve the scalper problem, since tickets can be assigned to individuals as opposed to code numbers when they are sold. The ticket sellers will distribute the smartcards to their registered members and assign the tickets to these smartcards when a member reserves a ticket. Instead of sending the tickets by mail or having the buyers pick up the tickets at a specific location, the buyers can use the smartcard as a ticket. When a registered member purchases a ticket, information about that user and his or her smartcard is stored in the ticket gates so that when the ticket buyer presents the smartcard at the ticket gate, he or she alone is allowed entry. Consumers will no longer have to pick up tickets and they will be able to purchase tickets much closer to the concert date than before. While previously it was hard to purchase concert tickets as the date of the event approached, smartcards will make same day ticket sales more common. This will also be beneficial to ticket sellers and promoters. Promoters do not want to be left with unsold tickets and thus may be willing to discount tickets at the last minute. While many radio stations give away unsold tickets, the Internet (in particular the mobile Internet) and smartcards will make it possible to vary the price of the ticket according to the demand as the concert date approaches. Of course, these benefits must be balanced against the costs of implementing readers, writers and smartcards. Silver screen Movie tickets represent about 20 percent of the tickets that are bought and sold in Japan. They are bought and sold in Japan in much the same way that they are bought and sold in the US. People line up to buy tickets at the movie theater and then line up again to enter the theater. As everyone knows, these lines are typically only a problem when the movie is very popular. Several firms such as Pia, Tsutaya Online and Kinema (in cooperation with Toshiba) are offering information on movie theaters including schedules on the mobile Internet, and some of them expect to begin offering reservation and smartcard services over the next couple of years. Pia and Kinema offer the most information on movie schedules and charge users JPY100 a month. For example, Pia offers what it claims to be real-time information including schedules on 2,500 screens, which is 80 percent of all the screens in Japan. The problem is that there are very few paying subscribers perhaps due to the easy access to the same information in magazines and the lack of genuinely real-time information. Theaters often change movie times and/or the number of screens showing a particular movie in response to demand, sometimes with little notice. This causes the published movie times to be incorrect, which is a problem that users do not expect to incur when they are using a supposedly real-time service on the mobile Internet. In fact, the largest movie theater chain, Warner Michael, has asked the movie information sites to refer all questions about movie schedules to its site since it doesn't like the complaints it receives from customers. However, official sites are not allowed to provide such linkages without DoCoMo's approval and this approval usually takes a long time. The lack of paying subscribers probably means that movie information sites need to adopt a different business model. Tsutaya Online's site is free to users; it does this to encourage video rentals and DVD sales on its site. Unlike the other sites, it also receives money from movie promoters to provide this information since it has more traffic than almost any other site in the Japanese mobile Internet. On the other hand, Pia operates its site and E-Plus plans to open a site in order to offer reservation services that include the use of smartcards. Movie ticket reservations may be difficult to do on the Internet. The former Ticket Saison (now E-Plus) tried to do this with Warner Michael but failed due to the incompatibility of their computer systems. This problem still probably exists. Another problem for ticket sellers is the low commission (10%), low prices (JPY1,500), and credit card charges (5%), which mean low profits for each ticket (about JPY75). Last month, we saw how with train tickets, the viability of Internet reservations increases as the price of the ticket increases. Odakyu has been able to introduce phones as tickets and capture all the costs and benefits, but movie tickets require firms to find some equitable distribution of them, which is often difficult. One way to profitably offer movie reservations is to offer them as a premium service, which is done by train companies in the form of charging extra for reserved seats. In the movie industry also, many people may be willing to pay for good seats and the right not to wait in line. Of course, it is only popular movies that are crowded and then generally only on weekends. It appears that most Japanese movie theaters are thinking less about premium services and more about how to fill their theaters on weekdays with discount tickets. Smartcards or phones containing them may be a necessary part of any reservation system. It is much easier for a movie theater to scan cards or phones than to physically manage the distribution of reserved tickets in the theater. Of course, the cost of card and phone readers may also be prohibitive. Movie theaters must balance the costs of implementing the new technology with the benefits of new revenues from ticket reservations. Further, they also need to consider the age of their main users (mostly young) and those who might be most interested in paying extra for reserved seats (older people). Phones as money DoCoMo's announcement on April 1 that it will use Edy in its phones brings us one step closer to an electronic money society. Credit card companies have been working on smartcards for more than 10 years and were expected to be the leaders in their implementation. The problem for credit card companies has been their high security needs and difficulties with convincing stores to implement new card readers and integrate them with point of sale (POS) systems. JCB, Japan's largest credit company with more than 38 million users and 8 million affiliates (along with Visa and MasterCard), began introducing credit cards containing contact-based IC chips in January 2002. These IC-based credit cards are potentially beneficial to stores, card companies and users. Stores can benefit from faster processing times and lower telecommunication costs since there is no need to confirm card validity. Instead, the card reader validates the information in the card and sends the purchase information to the credit card company. Information is only sent in the opposite direction when a card is stolen or invalidated. Credit card companies expect lower fraud and to be able to gather information about individual purchases. Individuals may also benefit from lower fraud along with customer-retention programs like point systems that provide heavy users with discounts or presents. While distributing these IC-based credit cards to its users is relatively easy, the challenge for JCB is to convince stores and other places of business to purchase new card readers and integrate the readers with their POS systems. The contact-based smartcards have higher security but at the expense of processing speed and cost as compared to non-contact cards. The cost of these cards and readers is more than double that of non-contact based cards and readers and may make it hard to persuade department stores, hotels and restaurants to purchase the readers. Thus, credit card firms may need to offer lower commissions in order to encourage stores to adopt smartcards. JCB believes it can reduce commissions, due to lower fraud with smartcards and the ability to gather information about individual purchases. It will be harder for people to utilize stolen cards since users must input a password when making a purchase. On the information side, although JCB will not be able to use or sell information about specific individuals, it can aggregate the product sales data gathered through the bar code reader and the individual data in the smartcard and sell it to its affiliated stores. One option is to offer lower commissions to those stores that have installed bar coders and POS systems. JCB is also offering its smartcards to firms such as airlines, although this requires readers in all airports. Japanese carriers could start with the Osaka to Tokyo route due to its high volume and then install readers in other airports. It could also be that these smartcards will play a role in greater airport security. JCB is promoting its IC-based credit cards as residence cards, medical insurance cards, medical record cards and passports, all of which obviously raise questions about privacy.  Convenience stores

Convenience storesIt is possible that convenience stores will move faster to install the necessary readers than will places of business that rely on more expensive purchases. Convenience stores can use non-contact smartcards since the purchase amounts are low, they are very concerned about processing times, they have the volumes to justify large investments and the stores have already installed POS systems. In fact, Japan's convenience stores probably have higher sales per square foot than any other type of store. They are located in areas that have the highest amount of pedestrian and car traffic -- the most successful stores are near train stations, where the pedestrian traffic is the highest. Their goal is to process payments as quickly as possible in order to keep the lines short and encourage more people to come into their stores. Several of Japan's largest convenience stores have already announced that they will implement equipment for handling smartcards. DoCoMo's announced adoption of Edy included a reference to am/pm's plan to introduce the equipment for handling Edy in 1,400 stores by July. Other stores want to introduce equipment that is compatible with smartcards to not only reduce checkout times, but also to promote their in-store multimedia terminals and ATMs. One question for convenience stores is whether their customers will want to use smartcards. Although consumers are accustomed to using credit cards and tickets when they ride trains or attend concerts, they are not accustomed to using cards or tickets in convenience stores. On the other hand, most convenience store customers are young and thus are major users of the mobile Internet, so DoCoMo's adoption of Edy in its phones may make them more comfortable with using electronic money in convenience stores. If non-contact smartcards or phones containing the smartcard functions are widely used in convenience stores before JCB's more sophisticated contact-based smartcards are used, it offers Bit Wallet and DoCoMo an opportunity to eventually challenge credit card companies. In the end, it is all about network effects. The more places people can use smartcards to make transactions, the more benefits there are to users. If people can use them to ride trains, go to concerts and movies, and do shopping, many people will adopt them, costs will come down, performance will rise, and the number of applications will expand.  The road ahead

The road aheadThe move towards Internet reservations and electronic tickets and money is accelerating. JR East's large number of users and complete management of the ticket system are major reasons why it has been able to introduce smartcards faster than other firms. The expected adoption by other JR companies and Hankyu in 2003 may provide sufficient network efforts to push the entire transportation industry towards smartcards by 2005. Greater use of smartcards as train tickets will lead to lower costs and greater demands for them from riders of both trains and buses. The problem of scalpers appears to provide the concert promoters and ticket sellers with sufficient motivation to introduce electronic tickets in the form of smartcards or IC chips in phones in 2002 or 2003. Although the number of users is certainly small compared to other applications like train, movie or sports tickets, the greater need will probably cause concert tickets to be an early application for smartcards and IC chips in phones. The use of smartcards and/or phones as concert tickets may provide the network effects to push the rest of the entertainment event industry towards them. It is possible that movie theaters and sports complexes will adopt the cards as early as 2005. Electronic money is of course the biggest potential market for smartcards and IC chips in phones. DoCoMo's use of Edy could very well start the ball rolling towards electronic money. But similar to JCB, NTT DoCoMo, Sony and the other partners in Bit Wallet must convince stores to adopt their technology. It appears that the promoters of Edy will have an easier time of this than JCB since their technology is less expensive and more appropriate for the probable first users of electronic money: convenience stores. It does not appear that there will be one winner in the use of electronic tickets and money. The Bit Wallet supporters are many and they are from a variety of industries including banks, smartcard and vending machine manufacturers, and even credit card companies. Even KDDI is a participant. JR will also most likely be a winner since its technology will most likely be adopted by a number of transportation companies and it is compatible with Bit Wallet's technology. But some firms will benefit more than others. Large railroad companies will find it easier than small railroads or bus lines to implement the new technology. E-Plus will probably benefit from smartcards being adopted as concert tickets more than the concert ticket sellers who depend on physical outlets for sales. Large convenience stores will probably find it easier than mom-and pop stores and restaurants to implement smartcards. The biggest question mark involves credit card companies and banks. At some point Bit Wallet's technology may offer sufficient security for expensive purchases and this potentially threatens JCB and other credit card companies like Visa and MasterCard that have not invested in Bit Wallet. Further, there are clearly larger implications for the spread of electronic money. Who needs cash when you can use smartcards and phones to make most of your purchases? Like all banks, Japanese banks have spent vast sums of money to build branches in areas with high human traffic and these investments may become unnecessary if people use less cash. More importantly, if the form of electronic money supported by NTT DoCoMo, Sony and others becomes popular, the entire concept of banking will change. It is no accident that Sony started a bank in 2001 and several Japanese banks are investors in Bit Wallet. Implications for the West Clearly, the early moves towards electronic tickets and money in Japan have major implications for the rest of the world. Granted, the use of electronic tickets and money will evolve in different ways in the rest of the world due to the lower importance of trains and convenience stores. For example, it is quite likely that entertainment events or even credit cards will be the early adopters of electronic tickets and money in the rest of the world. However, Japan's early implementation of electronic tickets and money may enable it to supply the technology to the rest of the world. Economies of scale and network effects will play an important role: The early use of these technologies in Japan will cause the costs of those systems supported by Japanese firms to drop faster than those supported by Western firms. Already, more than 12 million smartcards that are based on Bit Wallet's technology are used in Hong Kong's transportation system (called Octopus). It appears that electronic tickets and money will primarily be based on non-contact smartcards and chips in Japan. If improvements in this non-contact technology reach the level where it can be used in place of credit cards, non-contact smartcards and phones that use this technology may change the global market and not just the Japanese market for credit cards. @ Jeffrey L. Funk is an associate professor at Kobe University's Research Institute for Economics and Business Administration. |

|

Note: The function "email this page" is currently not supported for this page.

Magazine

For more magazine articles refer to our archives or view all magazines cover pages.

Tags

![]()

"To buy a sponsored link please send an email to info@japaninc.com"

Recent Comments

Employment in Japan

you don't understand at all

designboom article

Wow! - many thanks!

Property sites

Currencies

1 USD = 158.14 JPY

1 NZD = 93.64 JPY

1 AUD = 114.28 JPY

1 EUR = 184.63 JPY

1 GBP = 213.17 JPY

05/15/26 00:29 JST

1 NZD = 93.64 JPY

1 AUD = 114.28 JPY

1 EUR = 184.63 JPY

1 GBP = 213.17 JPY

05/15/26 00:29 JST

Links

BBC World News

- Warning of record global temperatures as chance of very strong El Niño grows

- 'Floating armoury' ship reportedly hijacked by Iran

- Flattery and fanfare as Trump welcomed to China - but thorny issues remain

- Former Nigerian minister sentenced to 75 years in rare corruption verdict

- Latvian PM resigns after row over stray Ukrainian drones