Make Deals or Die

Back to Contents of Issue: April 2003

|

|

|

|

by Sumie Kawakami |

|

Selling one's own corporation used to be considered an act of betrayal in Japan. But more Japanese corporations, big and small alike, are accepting this approach to survival as they look into opportunities to sell their non-core businesses under the new strategy of "select and concentrate." At the same time, stronger firms are looking into opportunities to acquire relatively healthy firms to strengthen their core businesses. With Japan's nonperforming loans hovering at historical highs, many corporate executives have come to view buyout activities as a viable means of survival. But industry sources admit that the buyout market has become over-crowded. In the first of our two-part series on buyout funds, we'll look at what players are doing to survive in this jam-packed market; in the second part, beginning on page 19, we'll take a close look at one of the more active buyout funds in Japan: Advantage Partners.

"It is not the strongest of the species that survive, nor the most intelligent, Japan's buyout market is only a few years old. 1997 marked the beginning of the market as we know it. Today, buyout funds are increasingly visible; pick up a Japanese newspaper and a buyout fund is likely to be mentioned as a potential bidder for one or another struggling company. Recent talks of Vodafone selling its fixed-line business, Japan Telecom, to Ripplewood Holdings, and of troubled Softbank possibly selling its shares in Aozora Bank to a foreign fund are just a few of the many examples. Final decisions in both cases had yet to be reached as of press time, but these cases are a clear indication that a partnership with a buyout fund is becoming a viable business option in Japan. Buyout funds are filling myriad roles today, too. Take a look at the recent management buyouts (MBOs) in Japan. Tower Records, Intuit (Japan) and many others have recently gained "independence" from their parents by forming MBOs with private-equity funds. At the same time, many market players admit that the buyout space has become over-crowded. Already several players have withdrawn from the market or have downsized their Japanese operations. J@pan Inc's January issue, page 30, predicted that some of the funds in play this year won't be around to ring in 2004, and the process of natural selection is already taking place. The Carlyle Group, one of the world's largest players with more than $13.9 billion in committed capital under management globally, recently downsized its Japanese operations. British buyout fund 3i Group is scheduled to close its Japanese office. When 3i entered the Japanese market in 1999, the company was expecting to do a few deals a year. But the only investment it made was one JPY15 billion buyout deal of former Nissan Motor distribution subsidiary, Vantec. As 3i's Tokyo representative, Mark Thornton, noted in a company press release: "Despite the possible long term potential in Japan, the buyout market has developed far more slowly than anticipated." Furthermore, Japan Equity Capital (J-Cap), a joint-venture private-equity fund by GE Equity (GE), Sumitomo and Daiwa Securities SMBC, planned to dissolve its entity by the end of March. Established in 2000, J-Cap has launched a JPY20 billion fund. It acted as an investment advisor for Meisei Electric when Daiwa Securities SMBC and others bought the company's shares from NEC, but J-Cap itself didn't close any deals, says company spokesman Toyoaki Kishihara. J-Cap operations will be Securities SMBC Principal Investments, a wholly owned subsidiary of Daiwa Securities SMBC, he says.

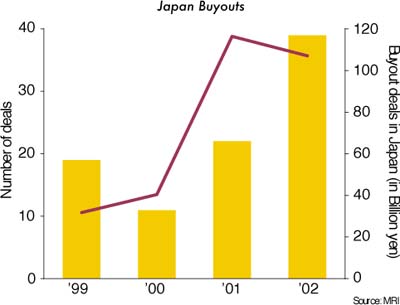

The quiet, smaller funds The most bullish are trying to squeeze money Yet many other funds have entered the market with the expectation that corporate restructuring and the rise in bankruptcies will push firms to sell their non-core divisions and improve their balance sheets. The continued weakness in the equity markets has been an impediment for buyout funds hoping to publicly list the companies they restructure, but it also keeps the prices of deals lower. Japan's zero-interest-rate policy also gives an additional incentive for leveraged buyouts (LBOs). Besides, the expected waves of industrial streamlining are supposed to give incentives to healthier corporations seeking out bits and pieces of these businesses at attractive prices. It isn't a good time for anybody to be raising funds. But the most bullish are trying to squeeze money out of investors who are hungry for high-risk, high-return opportunities. According to a survey by the Nihon Keizai Shimbun, Japan's leading business daily, corporate-restructuring funds specifically targeting Japan are poised to top JPY1 trillion in 2003. Since these funds normally acquire companies by combining their investments with two to three times the figure in loans through LBOs, they are likely to represent around JPY3 trillion in funding, the report says. Funds outnumber deals According to an MRI survey of major banks and private-equity funds in Japan, there were 39 cases of buyout activities in 2002, up from 22 a year earlier, while the total transaction volume shrank to JPY107.16 billion from JPY116.48 billion. Overall buyout activities have grown both in the number of deals and the transaction volume over the past few years. The number of deals in 2002 was almost double the number in 1999, while the volume grew threefold from 1999 to 2002. However, the Japanese market is still relatively small compared to the US and Europe. In the US, the total volume of buyout transactions was JPY2 trillion during the first half of 2002 alone. Although the negative image of buyout funds has diminished over the past few years, sellers are still skeptical of them and prefer to sell to other firms whenever possible, Kitamura says. Also, very few of these newly established funds have experienced staff, he says, as many came from venture-capital firms, the mergers-and-acquisitions business and consulting firms. While buyout activities normally require all of these skills, few are equipped with all the skills involved, he says. Most importantly, they tend to lack networks of people across different industries. "The ability to find good potential deals is crucial to the business. Access to corporations is the key," Kitamura says.

Winners and losers In order for buyout investments to gain profits, the acquired company needs to go public or be sold to a third party. While the climate has been unfavorable for initial public offerings (IPOs), Mizuho Capital succeeded in what was believed to be the first IPO of this kind. Japan Pure Chemical, which went through an MBO in 1999 in partnership with Mizuho Capital, went public on the Jasdaq market in December 2002. Its opening price was 30 percent more than its IPO price. In the meantime, MKS Partners has sold some of its shares in Xymax, a property management company it acquired from Recruit in 2000, and an athletic service firm, NAS , that it acquired from affiliates of the former Long-Term Credit Bank of Japan in 1999. MKS Partners' managing partner/CEO, Mobuo Matsuki, claims that its JPY17 billion Japan Venture Fund III, established in 1998, has returns of approximately 30 percent annually. MKS Partners, formerly Schroder Ventures, a joint venture established in 1985 between British financial institution Schroder and experienced venture-capitalist Matsuki, is known for having a broad range of expertise in hands-on investments. The firm became independent from Schroder and renamed itself in 2002. Industry sources say that Mizuho Capital, which used to be a member of the Fuji Bank group, accumulated know-how back in the 1980s, when "MBO" was a buzzword in Europe. Being a member of the Mizuho group, the firm is believed to have broad contacts with Japanese corporations. Advantage Partners is another firm that has a good record of exits (see the article beginning on page 19). IRC as a booster The details of how the revitalizing entity will work are still unclear. Especially unclear is who is to put the initial capital of JPY10 trillion on the table and whether the public entity will finish its job within five years. While some argue that the entire operation may prolong the suffering of certain ailing corporations unless the government sets a clear set of rules on who is to live and who is left to die, others say that the establishment of the IRC is at least an important step forward that will help boost buyout activities. "The Industrial Revitalization Corp. is really trying to act as an intermediary step between the banks and the funds or strategic sponsors," says Advantage Partners' Richard Folsom. "We had discussions with them about working together, where they would be looking to extract potential deals from bank portfolios and transfer those assets to funds like ourselves. So, from our perspective, that's not competition for a deal; it's actually a catalyst for additional deals," he says.

Public money in question Tokyo-based Phoenix Capital, for example, launched two funds last year to "revitalize" Japanese businesses, including a JPY20 billion "Japan Revival Fund" financed by domestic banks such as Tokyo-Mitsubishi, Mitsubishi Trust and the Development Bank of Japan. In the meantime, the Development Bank has agreed to invest in a few similar "revival funds," including one financed by Nippon Mirai Capital. Even MKS Partners will receive some capital from the Development Bank for its new JPY50 billion fund. But so far, these "revival funds" have seen little activity. However, Kitamura at MRI has some words of caution over the increased government involvement in buyout activities. "The beauty of private-equity funds," says Kitamura, lies in the fact that funds maximize returns via high-risk, high-return investments, and are therefore "highly motivated" to make things better. Pouring more public money into the system may water down their incentive, he says. Secondly, he says, it may also impede efforts by Japanese corporations to improve corporate governance. "Buyout activities normally work to strengthen corporate governance, as corporations are separated by the main-bank system." If a corporation is bought out by a fund invested in by the government or its main bank, it may lose incentive to change its organizational structure and speed up necessary reforms, although additional equities -- private or public -- may help improve their balance sheets. And foreign funds may make it harder to be part of the deal. @ |

|

Note: The function "email this page" is currently not supported for this page.

Magazine

For more magazine articles refer to our archives or view all magazines cover pages.

Tags

![]()

"To buy a sponsored link please send an email to info@japaninc.com"

Recent Comments

Employment in Japan

you don't understand at all

designboom article

Wow! - many thanks!

Property sites

Currencies

1 USD = 161.68 JPY

1 NZD = 93.19 JPY

1 AUD = 112.38 JPY

1 EUR = 184.63 JPY

1 GBP = 216.64 JPY

07/11/26 03:21 JST

1 NZD = 93.19 JPY

1 AUD = 112.38 JPY

1 EUR = 184.63 JPY

1 GBP = 216.64 JPY

07/11/26 03:21 JST

Links

BBC World News

- Superb Sinner ends Djokovic's latest bid for history

- Chip giant SK Hynix raises $26.5bn as shares surge in bumper US listing

- Zulu king expresses regret after video captures tirade against his wife

- Nolan Wells' family demands answers about US teen's death after boating trip

- US declassifies even more UFO videos