Japan's Digital Camera Industry

The Japanese domestic market for the digital still camera (DSC) will soon reach saturation. Market growth is slowing down and the drop in prices is changing the landscape of digital photography. This presents a challenge for many Japanese companies as they decide where to invest from now. Until recently, there were rapid advancements in technology, necessitating huge investments for the development of the digital camera. But with too many products available in major retail outlets in Japan, consumers have a hard time selecting a camera.

by by Nathalie Cavasin

It is now an era of survival for Japan's precision machinery industry in the DSC sector. "Made in Japan" DSC products could very soon become a thing of the past, as Japanese companies shift production overseas where costs are cheaper. The 'hollowing out' of the domestic DSC industry is inevitable. As a result, some Japanese companies have started to withdraw from the market while others are looking at merging technologies, investing in new areas or even creating new types of partnerships.

How the Digital Revolution Began

The transition from film to digital cameras was a technological revolution in the photography industry. The digital revolution in Japan began with what traditional camera makers called the 'Sony shock' in 1981. That year, Sony announced the first magnetic video camera, the Mavica, with a resolution of about 0.3 mega pixels. The electronic camera had a mini disc where images were recorded and stored. Late in 1989, Toshiba and Fuji Photo Film jointly developed the first digital electronic camera in the world. In 1995, Casio released the first consumer digital camera in the Japanese market, just as the film camera market was reaching the saturation point in 1996. (Until then, digital cameras were exclusively for professional photographers.) With the DSC, users could now store, edit and exchange digital photos. Japanese manufacturers lauded the digital camera as one of the so-called 'three sacred treasures,' along with the DVD recorder and the liquid-crystal display (LCD) television.

But by 2000, the rate of the digital camera's growth started to slow. According to the Japan Camera Industry Association (CIPA), in 2000 the domestic shipment of digital cameras was less than 3 million units. In 2003 it had grown 28 percent, but in 2004 domestic shipments were up only 1 percent (8.54 million units).

"This is the time when Japanese companies started to have trouble," says one general manager at Nikon. "All DSC began to have difficulties and could not make a profit."

Reaction to the Morphing of the DSC Industry

As one of the 'three sacred treasures,' the digital camera has been critical to the consumer electronics industry, but many DSC makers have started to experience excess inventories and deteriorating profits. Since sales have fallen, there are questions about the direction of these businesses.

One approach has been to reduce the stake in digital camera production. In April 2006 venerable Fuji Photo Film decided to remove 'Photo' from the company name, becoming 'Fujifilm.' Another company, Pentax, closed four of its seven sales bases in Japan. Since 2004, Olympus has also registered losses and for the first time, in 2005, closed domestic factories, having recorded a loss of JPY 23.9 billion in its camera business. In 2005, Kyocera decided to withdraw from the market.

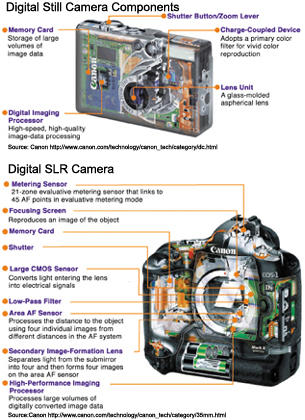

Konica Minolta is not only shutting down some operations but also transferring its remaining operations to other companies. The company suffered a JPY 8.7 billion operating loss in the photo-imaging sector during fiscal year 2004 and another JPY 7.1 billion loss during fiscal year 2005. As a result, Konica Minolta halted all worldwide operations in the photo-imaging business. The company transferred its Digital Single Lens Reflex (DSLR) operations to Sony in March 2006, shutting down the rest of its camera production. This is the first time Sony accepted a transfer of assets and facilities in electronics from another company. Sony has spent around JPY 20 billion to acquire Konica Minolta's digital camera business operation - a large investment considering the current difficult market in Japan. Sony is acquiring other companies to make up for technologies it lacks, as Canon once did. To become a top DSC maker, Canon made the strategic move in 1999 to purchase the semiconductor business of NKK (now part of the JFE holding group), in order to produce in-house the sensors that form the core of the digital camera. It was for the same reason that Canon acquired a metal-molds maker, which enabled it to internally manufacture the molds used in production. Today, Canon and Casio are the only camera makers still making a profit from the DSC.

For other Japanese camera makers, overseas markets beckon. Japanese manufacturers used to hold a 90 percent share of the global market, but the rate of growth has been declining in recent years. The battle is among many players. The reason lies in the modular nature of the DSC. Casio, for example, is developing only the LCD and acquiring all other core parts from competitors. In other words, Casio is focusing on its strengths - assembly and planning. The supply of core parts for other manufacturers creates a cooperative parts market, a market easy to access by companies that do not produce all the core the DSC components.

In 2004, shipments of Japanese companies still represented about 82.2 percent of the global share, or a total of JPY 1.5 trillion, according to CIPA. In 2005, there were about 30 DSC makers in the world. Sales in overseas markets are still expected to grow, but Nikkei BP Consulting forecasts an eventual decline in Japanese makers' share of the global market as US, South Korean, and Taiwanese companies start to invest in the DSC. However, the international DSC market will not mature for some years, and for the moment Japanese companies aim to expand sales in China and other emerging markets.

Hollowing Out

For now, Japanese companies are basing their R&D functions and manufacturing of high-level products, such as the DSLR camera, domestically. Canon, for example, manufactures its DSLR cameras in Japan. Some companies keep DSC production at home to safeguard intellectual property. According to Takatoshi Yamamoto, assistant director of the Industrial Machinery Division at the Ministry of Economy, Trade and Industry (METI), the Japanese strategy has also involved the management of a global-supply-chain, which includes factories in China.

Other companies have divided roles in the production process between Japan and China. Moving the assembly operations to China is a way to reduce costs. Fujifilm, besides downsizing its domestic operations, decided in 2006 to shift its entire DSC production to China. Up until now, the company had produced over 70 percent of its DSCs in China. Establishing a mass production system in China is part of Fujifilm's cost-minimizing structural reform of its electronic-imaging business. By 2005, Taiwan had secured around 41.8 percent of the global DSC market. However, 90 percent of its production was on behalf of Japanese camera makers. Japanese companies are starting to outsource production of low-end models to Taiwan.

The Digital Single Lens Reflex Camera and the Newcomers

With the shrinking of the DSC market in Japan, companies are looking to other investments. Some have aggressively invested in DSLR production. Lens makers such as Tamron and Sigma took the opportunity to develop new types of lenses for digital application when the traditional SLRs became digital. Camera makers have focused on the sales of interchangeable lenses and accessories. Pentax, for example, signed an agreement with Samsung, a South Korean manufacturer, to jointly develop DSLR cameras with these interchangeable lenses last October. Matsushita Electric also released its first DSLR camera in July 2006. Other companies are entering the market by providing products for the general user with no interchangeable lens.

Sony has just entered the DSLR camera market with a new product based on the Konica Minolta's Maxxun/Dynas mount. Such a development through using an outside brand is really an exception. Sony is now on the way to becoming a camera maker, but will they be able to compete with established leaders, such as Canon and Nikon?

Will the Cellular Camera Phone Replace the Digital Camera?

Although cellular camera phones are gaining popularity, they are still considered low-end compared with the DSC. While there was once discussion that the cellular camera phone would replace the DSC, such talk seems to have been premature. For one thing, phone makers have not solved how to equip their cameras with a zoom lens. For another, the phone camera has an incomparably shorter battery life than the DSC. Hiroshi Okazaki, vice president of the Communication and Information Network Association of Japan (CIAJ), explained, "As the cellular phone is having more additional functions, the increase of energy consumption needs a battery that has a longer duration."

Camera makers do not want to consider the business of mobile camera phones as a whole. A general manager at Canon says, "For a camera maker it is difficult to get into cellular camera phones. Japanese makers in that field are very aggressive, so it is difficult to compete with them...It is better for us to concentrate on the digital camera."

Some makers have, however, considered manufacturing the lens component for the phone camera. Fujifilm, for example, is planning to invest JPY 2 billion in a new plant in Tianjin, China, with a capacity of 5 million mobile phone camera lenses per month. The company holds around 60 percent of the global market share for manufacturing lenses for cell phones with over 1-mega-pixel resolution. Pentax also plans to produce in 2006 cellular phone camera lenses as part of a joint venture in China. The company will be using its expertise in digital camera lenses for manufacturing small plastic lens modules. On the lens manufacturers' side, Tamron will use its expertise in making DSC lenses to develop glass lenses for the camera phone lens mechanism. As the costs will be at least 30 percent higher than for the plastic lens mechanism, the company has justified the investment by banking on a growing market for the camera phone, particularly at the high-end segment. One general manager at Qualcomm Japan says, "In 2007, 3 mega-pixels will be mainstream for even mid-range phones. There should be a high-end phone with a 5-mega-pixel camera." The world market for cellular phone cameras is expected to grow from 130 million units in 2006 to 300 million units in 2009.

Preserving the Culture of Photography

After the DSC took off in the late 1990s, the demand for color film worldwide has been decreasing. Commented a general manager at Canon, "Because of digital, the culture of appreciating photos is beginning to disappear. There is not the need to print very much."

Camera makers are encouraging DSC users to print photographs by offering new services for photofinishing. Fujifilm, for example, created an alliance with Noritsu Koki (a pioneer of the minilab) in March 2006 to develop retail-printing services and to expand the opportunities in the digital-imaging field. There is a push to bring high-quality photography to general consumers.

Conclusion

So what are the strategies for Japanese precision machinery companies? Canon, which took the strategy to move toward the printing business and to enter the production of flat-panel TVs, is certainly setting a new direction for the industry in precision instruments. Fujifilm has decided to invest more in the medical imaging and life science sectors, as well as in biotechnology. Hiroshi Okazaki, vice president of the CIAJ, likened the current DSC situation to the story of the calculator and PC in Japan. In the latter cases, only very few companies could stay in the calculator or PC businesses because of the strong competition. The situation is similar for digital cameras. They are an example of a product with modular architecture. With the opportunity to select and assemble components, many Japanese companies other than traditional camera makers have entered the field. Modularization boosts productivity and lowers production costs. It could be possible that only a few manufacturers remain, as some analysts foresee more mergers. According to an article in the June 5th, 2006, edition of the Nikkei Weekly, Pentax may consider a merger, as it is increasingly difficult to stand alone in an industry with many players. There is the question today of how Japanese companies can remain profitable with modular products. Apple's success with the iPod, which focuses on downloading music content, is one example of innovation in modular architecture. Japanese companies have strengths in higher technology but they now need to improve their competitiveness in modularization by focusing more in the future on design and brand power on a global stage. JI

Nathalie Cavasin, PhD, is a visiting researcher at the Global Information and Telecommunication Institute (GITI) of Waseda University. Any views and opinions expressed in this article are those of the author only and do not represent or reflect the views of the GITI.

Selected references:

Camera & Imaging Products Association (CIPA), Camera Industry in Japan, CIPA report 2005, Tokyo.

Ikeda (N.), "The Pitfalls of the Digital Appliances Bubble," column, January 13, 2004, RIETI, Tokyo.

The Nikkei Weekly, "Maturing Markets Invite M&A Deals," June 6, 2006.

Yamamoto (T.), "Why Does Japanese Camera Industry Win in the World?" Slide presentation, METI, Industrial Machinery Division, August 2, 2006.

Magazine:

Magazine

For more magazine articles refer to our archives or view all magazines cover pages.

Tags

![]()

"To buy a sponsored link please send an email to info@japaninc.com"

Recent Comments

Employment in Japan

you don't understand at all

designboom article

Wow! - many thanks!

Property sites

Currencies

1 USD = 162.60 JPY

1 NZD = 93.71 JPY

1 AUD = 112.08 JPY

1 EUR = 183.85 JPY

1 GBP = 214.79 JPY

07/31/26 05:25 JST

1 NZD = 93.71 JPY

1 AUD = 112.08 JPY

1 EUR = 183.85 JPY

1 GBP = 214.79 JPY

07/31/26 05:25 JST

Links

BBC World News

- Migrants seen swimming around border fence of Spanish enclave Ceuta

- Danube's record low levels force shutdown of Hungary's only nuclear plant

- Father of teen school shooter sentenced to 15 years in prison

- Why limited war with the US may suit Iran better than peace

- Hundreds of migrants swim from Morocco to Spanish enclave of Ceuta