Office Landlords Back on Top as Vacancy Falls in Central Tokyo

Back to Contents of Issue: April 2005

|

|

||

|

by Dylan Robertson |

||

Much has changed in the office market since early 2003, when the market was flooded with new Grade A office supply, and tenants were offered favorable rents and enticing concessions. Today many companies are well positioned, having taken advantage of the opportune market and upgraded to new buildings. Almost all of the new space that alarmed market watchers to warn of "2003 Problem" has now been absorbed. Much has changed in the office market since early 2003, when the market was flooded with new Grade A office supply, and tenants were offered favorable rents and enticing concessions. Today many companies are well positioned, having taken advantage of the opportune market and upgraded to new buildings. Almost all of the new space that alarmed market watchers to warn of "2003 Problem" has now been absorbed.

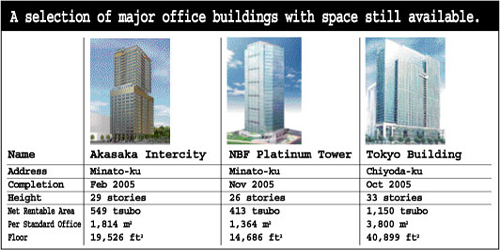

Strong occupier demand for new office product and a relative tightening of new supply have combined to squeeze vacancy in Grade A offices to its lowest since the fourth quarter of 2001. So the balance of power in lease negotiations is shifting back towards landlords, and the recent public announcement of Mori Trust, a major developer, to raise rents across its portfolio is confirmation of the trend of improving landlord sentiment. The decrease in vacancy rate and the firming of rents comes at a time when, despite the recent increased optimism in Japan's economy, a great number of businesses are still looking to restructure and reduce costs. Take-Up Although only one Grade A building, Mori's Holland Hills project, near Kamiyacho Station in Minato Ward, was completed in the fourth quarter of 2004, adding 4,154 tsubo (13,732 m2 = 147,810 ft2), demand for existing pockets of Grade A vacancy remained brisk. Pent-up demand from international and domestic companies for modern office space with large floor-plates has caused Grade A vacancy to plummet from 8.8 percent in mid-2003 to the current level of 3.6 percent. A total net take-up of Grade A offices of 235,971 tsubo (780,000 m2 = 8,395,850 ft2) was recorded across the Central Five Wards in 2004. This was the second highest total, only marginally lower than the record of 237,786 tsubo (786,000 m2 = 8,460,434 ft2) in 2003. Much of the leasing activity in 2004 was focused on the overhang supply of Grade A buildings completed in Minato and Chuo Wards in 2003. Many of these buildings are now at or approaching full capacity. Rentals The tightening of availability in Grade A stock in the last two quarters of 2004 has encouraged landlords to raise their rental expectation levels by 5-10 percent, particularly in premium buildings in core office locations. As yet, this trend has not filtered through to Grade B and C buildings. Rents in smaller premises in the leading Grade A buildings are rising at a more rapid rate. Gross asking rental rates (including common area management fees) for prime buildings in the Marunouchi area, near Tokyo Station, are now approaching \50,000/tsubo (\15,125/m2 = \1,405/ft2) per month. Using an exchange rate of 1 USD = 105 JPY, this is equivalent to US$161/ft2/year. Central Tokyo currently has the world's second highest rents after central London. New Supply New Grade A supply in central Tokyo will drop to 99,834 tsubo (330,000 m2 = 3,552,090 ft2) in 2005, 20 percent lower than in 2004. However, over 75 percent of this office product has already been pre-committed. This means only 24,958 tsubo (82,500 m2 = 888,023 ft2) of new office space will be available in 2005. This is only 10.5 percent of the amount of new supply absorbed in each of the last two years. Since mid-2004, there has been an increased willingness among tenants to commit to buildings ahead of their practical completion, particularly if the developer is renowned for its high-quality product. If this trend continues, it will likely have four effects: constructed before 1982 with high technical specs or upgraded; these buildings make up approximately 10 percent of the total Five Ward office stock.) The remainder of the Tokyo office market (approximately 65 percent) consists of small-floor-plate buildings in secondary locations. Demand for this stock remained largely unchanged in 2004; however, the strength of the Tokyo residential market coupled with flexible zoning regulations will likely cause Grade C office stock to decline in the mid-long term. 2005 Forecast Although there is growing concern about a possible slowing of the Japanese economy, the current status of the Grade A market, with low levels of vacancy, limited new supply, and strong levels of occupier demand, indicates that it will be vulnerable to a potential downturn. Real estate agents are still experiencing strong interest from tenants for new office product, and given the limited new supply and scarcity of large contiguous spaces in existing buildings, they expect early commitments to new buildings to continue. Consequently, Grade A vacancy should fall below 3 percent by the end of the second quarter of 2005. Falling vacancy has already reduced concessions landlords offer tenants to lease new buildings. Capital contributions for major commitments at new buildings, prevalent in the first half of 2004, have all but disappeared, and rent-free periods for fixed term leases of five years or more have fallen from 10 - 12 months to as little as 4 - 6 months. I anticipate rent-free concessions for new buildings will soon be reduced to the typical two-month fit-out period. Concessions at existing buildings are likely to remain at four to eight months in 2005, depending on the level of vacancy in the building. I anticipate two possible scenarios for effective rentals (calculated by spreading the effect of rent-free periods over the initial term of the lease) in 2005: (1) If the local economy continues to remain strong and tenant demand is unaffected, effective rents in Grade A buildings could rise by 15 to 20 percent. I rate this as a 20 percent likelihood. (2) If economic growth slows, I am more conservative about rental increases, which I estimate between 5-10 percent. I anticipate this is a more likely scenario at 80 percent. Companies looking for value may have to consider existing buildings. Regardless, tenants would be well advised to review their real estate strategies. @

|

||

Note: The function "email this page" is currently not supported for this page.

Magazine

For more magazine articles refer to our archives or view all magazines cover pages.

Tags

![]()

![]()

"To buy a sponsored link please send an email to info@japaninc.com"

Recent Comments

Employment in Japan

you don't understand at all

designboom article

Wow! - many thanks!

Property sites

Currencies

1 USD = 154.50 JPY

1 NZD = 91.05 JPY

1 AUD = 99.23 JPY

1 EUR = 164.19 JPY

1 GBP = 192.30 JPY

04/16/24 18:28 JST

1 NZD = 91.05 JPY

1 AUD = 99.23 JPY

1 EUR = 164.19 JPY

1 GBP = 192.30 JPY

04/16/24 18:28 JST